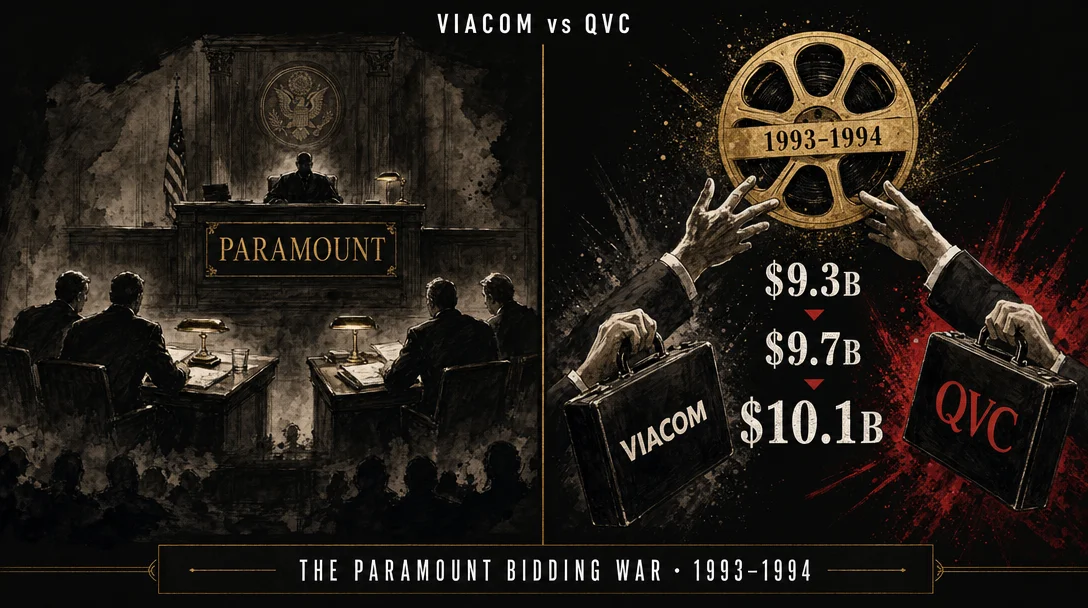

"The deal from Hell": how the Paramount bidding war rewrote every M&A board's duty

In September 1993, Viacom and Paramount announced a friendly merger. Eight days later, Barry Diller's QVC launched a hostile counterbid that triggered five months of lawsuits, wiretapping allegations, and escalating cash bids — from $69/share to a $9.7 billion final price. The case traces the full arc from Redstone's strategic motivation, through the three contractual lockups the Paramount board granted Viacom (stock option, no-shop, $100M termination fee), the Delaware courts' twin rulings that invalidated those provisions, and Viacom's Blockbuster-funded financing rescue, to Redstone's champagne toast at restaurant "21" on February 15, 1994. It closes with three reusable frameworks: Competitive Arousal (Malhotra/HBR 2008), Negotiauctions (Subramanian/HBR 2009), and the Revlon lockup trap.

Why Redstone needed Paramount

Parties and leverage

| Sumner Redstone / Viacom | Martin Davis / Paramount board | Barry Diller / QVC | |

|---|---|---|---|

| Stated objective | Acquire Paramount's studio and library; build the second-largest U.S. media company | Execute the Viacom merger on agreed terms; deliver a premium to shareholders | Outbid Viacom; return Diller to the studio he had run from 1974 to 1984 |

| Hidden objective | Lock in Paramount before any rival could intervene; preserve Biondi as a future operator | Keep Davis in an executive role post-close; avoid a public auction that could derail the deal | Use Comcast and John Malone's TCI as financial backing to credibly threaten Viacom |

| BATNA | No meaningful alternative: Viacom without a studio faced long-term distribution vulnerability | Continue as an independent but vulnerable standalone — the 1989 restructuring had not solved the scale problem | Walk away with minority cable holdings; Malone retained his TCI empire regardless |

| Key leverage | Signed deal with three protective lockups (stock option, no-shop, $100M termination fee); first-mover advantage | Signed merger agreement; incumbent management; access to Lazard as financial advisor | Higher per-share offer (eventually $90/share vs. Viacom's $85); deep-pocketed backers |

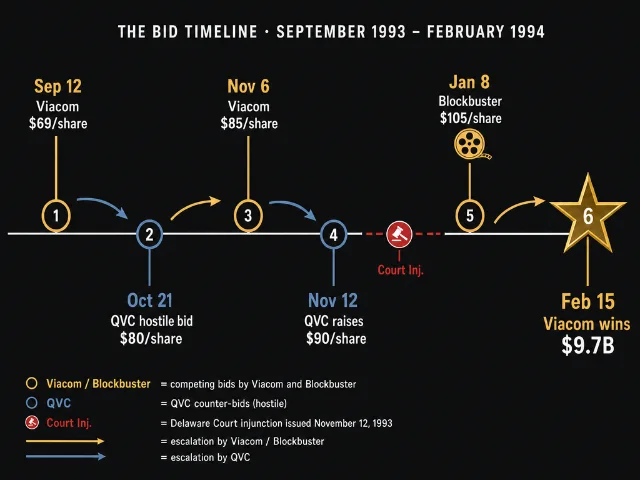

The hostile bid and the war's first shots

How the board lost control: the three lockups

- The Stock Option Agreement: Viacom received an option to purchase 19.9% of Paramount's shares at $69.14 per share. The option could be paid with a subordinated note (no need for Viacom to raise $1.6 billion in cash), and Viacom could alternatively demand that Paramount pay the difference between the option price and the market price in cash. The Delaware courts called these features "draconian." 2

- The No-Shop Provision: The board agreed not to solicit, encourage, or respond to competing bids. Combined with the stock option, this made it structurally rational for Paramount shareholders to accept the lower Viacom bid rather than wait for a process that management was actively suppressing.

- The $100 million Termination Fee: Payable to Viacom if the deal fell apart under certain conditions.

The Blockbuster gambit

What Delaware actually decided

"When a corporation undertakes a transaction which will cause: (a) a change in corporate control; or (b) a breakup of the corporate entity, the directors' obligation is to seek the best value reasonably available to the stockholders." 2

Victory at "21"

Frameworks you can use

1. Competitive arousal: why rational bidders stop being rational

- Intense rivalry: one-on-one competition is uniquely activating. Redstone and Diller had a history. They had been friends. The bid felt personal.

- Time pressure: court-ordered deadlines on each bid cycle created artificial urgency that made walking away cognitively harder.

- Spotlight: a bidding war for a Hollywood studio, covered daily by the press, with shareholders watching — every move was visible.

2. Negotiauctions: when you stop choosing between deals and auctions

3. The Revlon lockup trap: three devices that individually survive scrutiny but together destroy it

- Termination fees in reasonable amounts (generally up to 3–4% of deal value) have been approved by Delaware courts in change-of-control settings.

- No-shop provisions with a "fiduciary out" — allowing the board to respond to genuinely superior offers — have generally survived scrutiny.

- Stock options at a limited percentage of shares (below 20%) have been used as deal-protection mechanisms.

What to remember

- The trigger for Revlon duties is control transfer, not corporate break-up. Before Paramount v. QVC, boards in many friendly mergers argued that Revlon only applied when the target was being broken up. The Delaware Supreme Court closed that argument permanently: any transaction that places a company in the hands of a single controlling shareholder — as opposed to widely dispersed public stockholders — activates the board's obligation to seek the best available price. 2

- Boards cannot contract away their fiduciary duties. Viacom argued that the stock option and no-shop provision represented vested contractual rights that could not be undone by a competing offer. The court rejected this argument directly: a board that grants provisions inconsistent with its fiduciary duties has not created a valid contract — it has created an invalid one. 2

- The standard is process, not just outcome. The Delaware courts did not simply compare the two bids and pick the higher one. They examined whether the board's process for evaluating bids — the documents distributed before the November 15 meeting, the restrictions placed on Lazard, the failure to ask any independent questions about QVC's financing — was reasonable. 4 A board that produces a reasonable outcome through an unreasonable process can still face legal liability.

- The winner's final price reflects the competition, not the strategy. Redstone's original bid was $69.14 per share. His final winning bid was approximately $9.7 billion in cash and securities. The bidding war forced by QVC's entry — which Redstone called "the deal from Hell" — added over $1.5 billion to the price he ultimately paid. The same competitive dynamics that Malhotra and colleagues identified as "competitive arousal" in HBR also drove QVC's escalating bids. Both sides paid more than they planned to at the outset. 8

- Financing is a strategy, not just logistics. Viacom's Blockbuster gambit was not a signal of weakness — it was a rearmament. When Nynex's capital became unavailable, Redstone found an alternative source in six weeks: a $8.4 billion merger with a company Blockbuster's chairman wanted to get off his hands. The deal created a new problem (the company had nearly $10 billion in debt after close), but it solved the immediate one. Bidders who enter auctions without a clear financing alternative for a higher-than-expected clearing price frequently lose deals they should have won.

References

- 1The New Yorker: Redstone's Secret Weapon

- 2Delaware Supreme Court: Paramount Communications Inc. v. QVC Network Inc., 637 A.2d 34

- 3Wikipedia: Paramount Pictures

- 4Delaware Court of Chancery: QVC Network, Inc. v. Paramount Communications Inc., 635 A.2d 1245

- 5The New York Times: Viacom to Merge With Ally in Bid for Paramount

- 6The New York Times: Viacom Is Winner Over QVC in Fight to Get Paramount

- 7Wikipedia: Sumner Redstone

- 8Harvard Business Review: When Winning Is Everything

- 9Harvard Business Review: Negotiation? Auction? A Deal Maker's Guide

Add more perspectives or context around this Drop.